The Dip in SEA Fintech Funding: What Startups Can Learn

Fintech AI Startups Early Startups SEA 4 Minutes

Startups can learn from the recent SEA fintech funding dip that capital has not disappeared; it has simply become more selective. Investors now prioritize sustainable, compliance-aware growth, investor-grade financial modeling, clear monetization, and thoughtful capital-stack design, creating an opportunity for prepared founders to stand out, raise efficiently, and secure better-quality partners.

A new funding playbook for SEA fintech

Scoreboard, end of Q3 2025: Southeast Asia’s fintech market is playing defense. Deal volume across the region hit a multi-year low in the third quarter, with just 112 startup equity deals, the weakest quarterly tally in more than six years, even as a single mega-transaction skewed total dollars raised. Late-stage rounds showed a modest rebound, but early-stage activity thinned further.

Zoom out to the season-to-date numbers and the slump looks even starker for fintech specifically. In the first nine months through 30 September 2025, ASEAN fintech funding fell 36% to about US$835 million, with deals down 60% to 53, the lowest funding and deal count since 2016. Yet the average deal size rose 42% to US$21.4 million, and late-stage rounds captured 67% of total capital, clear signs of capital concentrating around scaled, resilient players. Singapore took the lion’s share, at 87% of funding.

Global context matters for the scouting report. Worldwide fintech dollars were roughly flat quarter-over-quarter in Q3, but more capital clustered in US$100M+ rounds, a pattern that mirrors the selective deployment we are seeing in Southeast Asia.

From blitzscaling to disciplined execution

Investors are now rewarding fintechs that can prove profitability, scalability, and sustainability, not just user growth. In Q3 regional data, the bright spots were late-stage companies with clearer paths to cash flow, while early-stage pace slowed and screening tightened.

Several investors also highlighted governance and operating discipline, not storytelling, as the new baseline. Growth still matters, but in 2025 it has to ride on top of clean books, controlled risk, and business models that can withstand regulatory and macro shocks.

Private debt is still on the field

Even amid the equity squeeze, private debt remained relevant in Q3, particularly for later-stage companies with strong financials and clear monetization. The difference is that lenders have raised the bar: they want robust balance sheets, tight reporting, and clear recovery metrics.

Debt is still in play, only now it is more selective and heavily data-driven. For founders, that means a well-designed capital stack can combine equity and credit to extend runway and reduce dilution, if the numbers support it.

The Investor-Readiness Playbook

Think of this as tightening your defensive line before you press the offense.

What does investor-grade financial modeling look like now?

-

12 to 24 month runway with weekly cash tracking and a clear contingency plan (cost levers, hiring gates).

-

Cohort-level unit economics (LTV/CAC with cash payback) and product-level contribution margins that reconcile to GAAP or IFRS P&L.

-

Credit and risk modeling if you touch lending or spread: expected loss (IFRS 9 style), vintage curves, roll rates, collections efficiency, fraud loss rates, and interest-rate sensitivity.

-

Regulatory capital and liquidity implications for your license class (for example, MPI, lending, brokerage) embedded in the plan, not parked in side decks.

-

Scenario analysis aligned to today’s funding market: base, conservative, and “no new equity” cases, all showing deleveraging of burn and a path to breakeven.

Why it matters now: Late-stage dominance and larger average checks show investors are concentrating bets. Your model must prove durability, not just growth.

Governance that reduces risk and the cost of capital

-

Board hygiene: an independent director with risk or compliance experience, a standing Audit and Risk committee, and DACI or RACI frameworks for key decisions.

-

Compliance by design: AML and CFT policies, transaction-monitoring procedures, suspicious-activity escalation logs, and third-party KYC or AML vendor oversight.

-

Data and security posture: access controls, incident response runbooks, and progress toward SOC 2 or ISO 27001, backed by evidence, not aspirations.

-

Revenue recognition and controls: clear policies for fees versus float, interchange, rebates, and incentives, plus reconciliations to bank and processor statements.

Why it matters now: Investors explicitly cite governance and tangible operating performance as differentiators in Q3 diligence. Clean governance can lower diligence friction and increase debt capacity.

Monetization that is obvious and compliant

-

One crisp primary revenue engine (spread, interchange, SaaS fee, take-rate) with sensitivity to regulatory changes and partner-bank policies.

-

Attach and cross-sell metrics by cohort: ARPAC or NRR for B2B and product attach rates and churn for consumer.

-

Unit economics at steady state, not just launch promos, plus proof you can scale without inflating fraud losses or chargebacks.

Why it matters now: With capital concentrating in fewer, larger rounds, investors are picking models that scale revenue without excess compliance or fraud risk.

A 2025-ready capital-stack strategy

-

Map the equity and private credit mix: what you will fund with non-dilutive capital (receivables, working capital facilities, revenue-based financing) versus equity.

-

Prepare lender-grade data tapes (aging, defaults, recoveries, fraud cohorts) alongside your equity data room.

Why it matters now: Private debt is still in play for companies with disciplined books. It can extend runway and reduce dilution if your metrics support a compelling debt facility structure.

A dataroom that speeds investor “yes”

-

Monthly P&Ls with bank or processor reconciliations; a KPI dictionary; cohort files (acquisition channel by product by country); and compliance evidence (policies, audits, SAR summaries).

-

Customer concentration analysis, top contracts (with term sheets), partner-bank agreements, and regulatory correspondence, so there are no surprises.

One-Month Training Camp for Fintech CFOs and CEOs

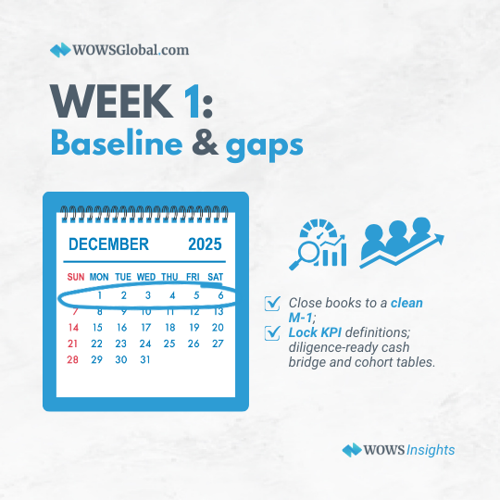

Week 1: Baseline and gaps

-

Close books to a clean M-1.

-

Lock KPI definitions.

-

Build a diligence-ready cash bridge and cohort tables.

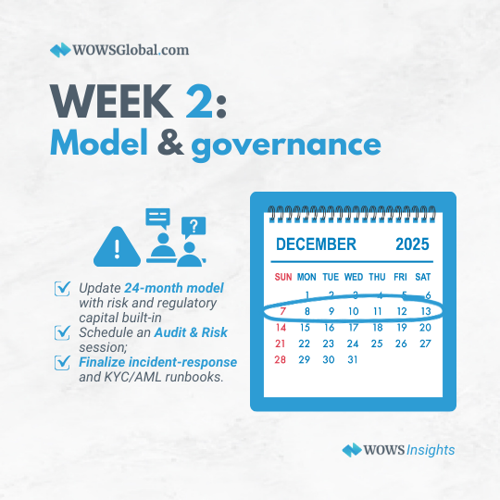

Week 2: Model and governance

-

Update the 24-month model with risk and regulatory capital built in.

-

Finalize incident-response and KYC or AML runbooks.

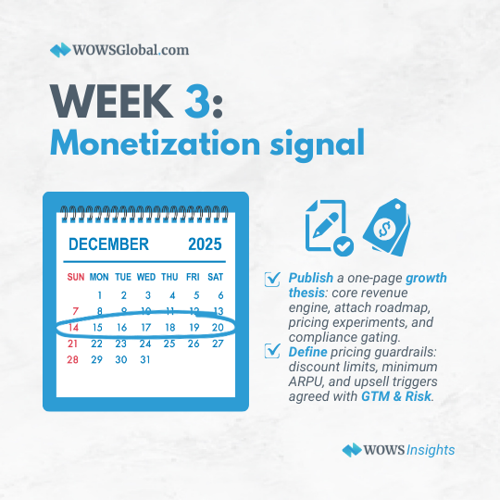

Week 3: Monetization signal

-

Publish a one-page growth thesis: core revenue engine, attach roadmap, pricing experiments, and compliance gating.

Week 4: Capital stack and materials

-

Build the lender data tape.

-

Map five credible debt facility options.

-

Refresh the investor memo with updated unit economics, governance evidence, and use of proceeds.

How WOWS Global can support your next raise

Investor-grade financial modeling

Cohort-based LTV/CAC, IFRS-aligned P&L bridges, risk-adjusted lending models, and scenario packs that your board can sign off on.

Dataroom and story preparation

KPI dictionary, reconciliation workflows, and a cohesive investor memo plus dataroom that anticipate the questions equity and debt investors will ask.

Curated investor introductions

Warm introductions to aligned venture and private-capital investors whose stage, ticket size, and thesis match your profile, so you spend more time in high-fit conversations, not cold outreach.

Debt facility and private-credit support

Guidance on structuring your debt facilities, preparing lender-grade data tapes, and positioning your metrics so you can engage relevant private-credit providers from a position of strength.

WOWS’ Take: Discipline wins in a selective fintech market

This market is not uninvestable, it is unforgiving. Q3 data shows that capital is still on the field, but it is playing fewer hands with stricter rules. If your numbers, governance, and monetization are game-ready, you can still move the chains. In a selective market, discipline is the edge.

WOWS Global helps you sharpen your financials, optimize your capital stack, and build an investor-ready dataroom. Schedule a call to get started.

FAQs

Why did SEA fintech funding dip in Q3 2025, and what does it signal?

The slowdown reflects a reset from “grow at all costs” to disciplined, compliance‑first execution. Capital hasn’t left; it’s concentrating in fewer, larger late‑stage bets with credible paths to profitability. For early‑stage teams, screening is stricter and narrative‑only pitches are out; investor‑grade numbers, governance and monetization clarity now determine who gets meetings.

What metrics and controls do investors expect to see today?

Investors want decision‑quality data and provable unit economics: cohort LTV/CAC with cash payback, contribution margins reconciled to GAAP/IFRS P&L, and a burn multiple trending down. For lending models, show loss vintages, roll rates, and collections. Pair that with board hygiene, AML/KYC controls, audit‑ready reconciliations, and progress toward SOC 2/ISO 27001.

How can a fintech become investor‑ready in 30 days?

Week 1: close books cleanly, lock KPI definitions, map runway. Week 2: rebuild the 24‑month model with risk and regulatory capital; schedule Audit & Risk. Week 3: sharpen one primary revenue engine and pricing; document compliance runbooks. Week 4: assemble the data room and lender data tape. WOWS Global can facilitate each step end‑to‑end.

Related Posts

-

Retail Investors AI Startups Southeast Asia 4 Minutes

Polarlyst: The Thai AI “Co-Pilot” Bringing Institutional-Style Research to Retail Investors

Polarlyst is a Thai AI-driven investing “co-pilot” turning complex financial data into clear, actionable insights for retail investors. In this WOWS Global spotlight, we break down why they stand out, why they’re worth watching, and what their rise says about the next wave of WealthTech in Southeast Asia. -

Early Startups Fundraising Due Diligence Data Room

2026 Fundraising: What Changed?

Fundraising in 2026 isn’t about moving faster—it’s about showing up prepared. Learn how to build an investor-ready system (modeling, governance, data room, and investor fit) so diligence doesn’t drag and your strongest conversations go the distance. -

Fintech SEA AI Startups Early Stage 5 Minutes

Moonshot Ventures: Betting Early on Southeast Asia’s Purpose-Driven Builders Starting with Women-Led Innovation in Indonesia

Moonshot Ventures invests early in Southeast Asia’s most mission-driven founders, pairing capital with deep operating support. Through IWEF, it’s helping women-led innovation in Indonesia scale with a tranche-based model and a strong partner network. -

Capital SEA B2B ASEAN 7 Minutes

Cocoon Capital: Backing Southeast Asia’s Quiet B2B Revolution

From AI-powered stroke diagnostics to pharma distribution and SME payment rails, Cocoon Capital backs the “invisible” infrastructure powering Southeast Asia’s next wave of growth. This Investor Spotlight unpacks their B2B and deep-tech thesis, how they invest, and the founders they champion. -

Tourism Travel SEA Tech 5 Minutes

Yacht Me Thailand: Digital Yacht Charter Platform for a Fragmented Market

Yacht Me Thailand is digitising yacht and boat charters across Thailand’s top marine destinations. With operator-first tools, sustainability at its core and ambitions to become a regional boating OTA, the platform is emerging as a notable travel-tech and marine tourism play. -

Series B Singapore SEA India 5 Minutes

Iron Pillar: Scaling India-Built Tech Into Southeast Asia

Iron Pillar is a venture-growth firm backing India-built technology as it scales across Southeast Asia. This spotlight covers stage focus, typical checks (US$5–15M), sectors, SEA go-to-market via Singapore, and notable portfolio patterns in SaaS and platforms. For founders and co-investors, it’s a practical guide to where Iron Pillar fits, and how to engage.